The Top 50 Lower Middle Market Consumer Investors & M&A Advisors

The polarized economic performance of the Consumer industry over the last 9 months has all the makings of a great…

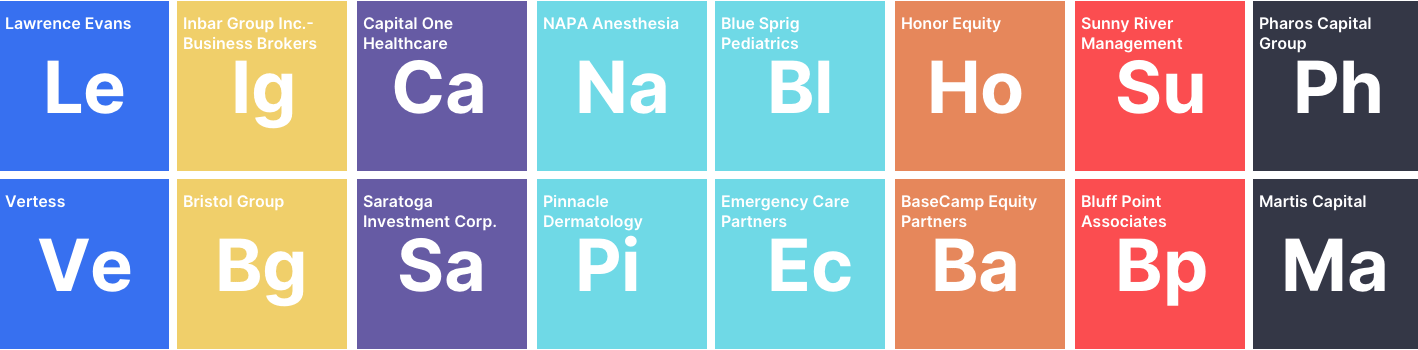

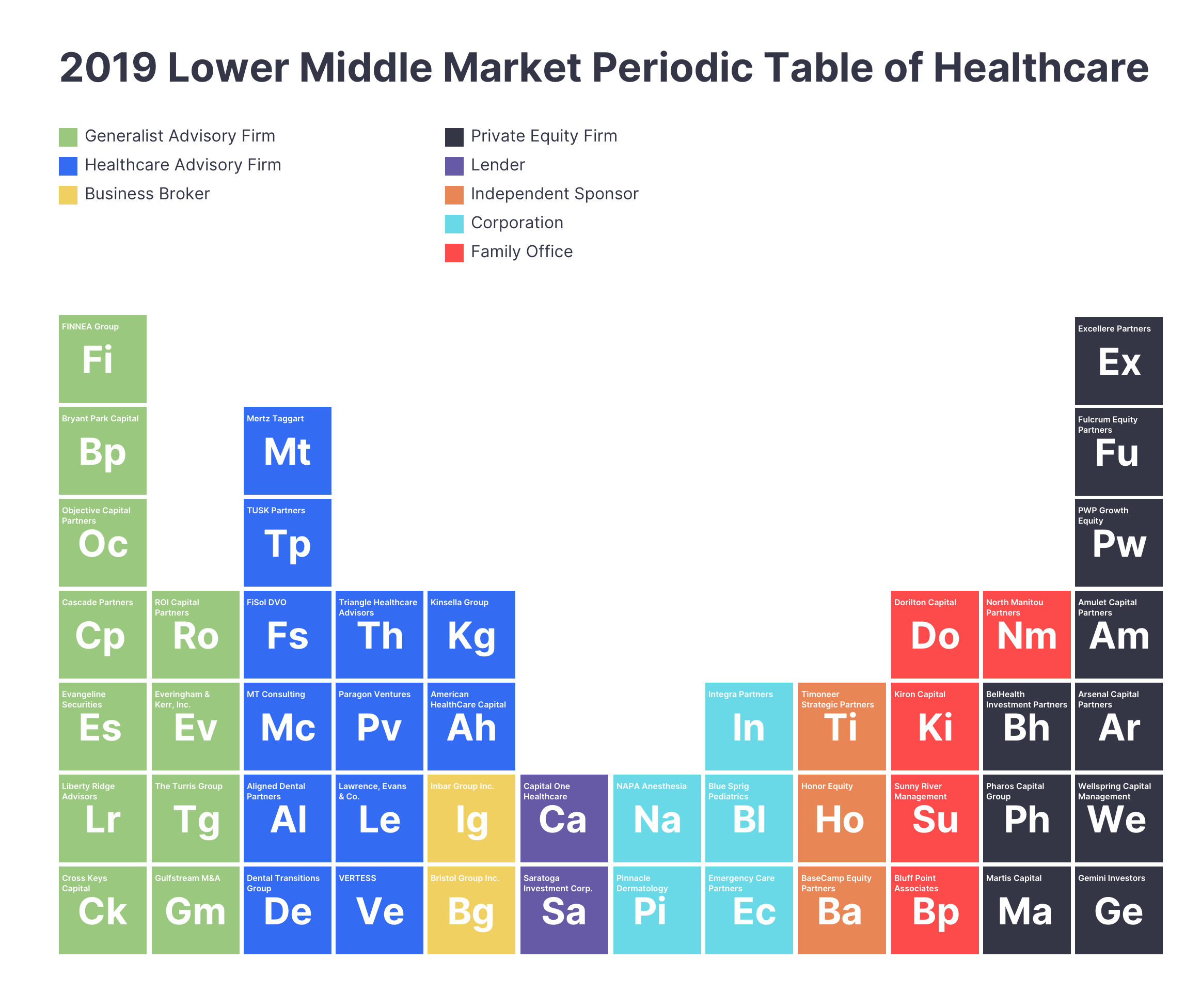

Who are the most active healthcare investors and advisory firms in the lower middle market today? In Axial’s 2019 Lower Middle Market Periodic Table of Healthcare, we unpack insights from proprietary private transaction activity on Axial to determine not only which players dominate the space, but which healthcare sub-sectors are seeing the highest levels of current demand (rather than historical closure data) from financial investors and corporate acquirers.

We borrow heavily from CB Insights, a leading market research firm, who pioneered the periodic table approach analyzing industry categories and their most important players. Our periodic table below reveals Axial’s 25 most active lower middle market healthcare investors and acquirers, and 25 most active healthcare investment banks and advisory firms.

The data driving the periodic table incorporates member closed transaction data, as well as Axial platform activity that assesses firms’ healthcare experience and specialization benchmarked against 5,000+ of their peers. We’ve also included a full report below with commentary and analysis from these top Axial members on sector trends and forecasts.

This is the first report in an ongoing series, and we’d love to hear your feedback. Email us at [email protected] If you have questions, ideas, or additions.

50 top lower middle market executives and deal professionals in healthcare (see full list below)

50 top lower middle market executives and deal professionals in healthcare (see full list below)

Introduction

National health spending in America is projected to grow at an average rate of 5.5 percent per year for the next 10 years, reaching nearly $6.0 trillion by 2027, according to the Centers for Medicare & Medicaid Services.

The aging American population is the industry’s primary growth driver. According to projections from the U.S. Census Bureau, the number of people over 65 will grow from 43 million in 2012 to 84 million by 2050, rising from 14 percent of the population to 21 percent, reports AMN Healthcare. As people age in affluent countries like the US, they need greater quantities and greater complexity of healthcare services – both of which drive growth in healthcare spend and healthcare labor requirements.

Healthcare presents an interesting category of transaction activity for lower middle market market investors and acquirers: cash flows in many healthcare categories are largely uncorrelated to economic cycles; labor-centric business models present substantial opportunity for operational improvements to increase profit margin; and significant fragmentation creates an opportunity for repeatable roll-up programs.

Sizing Up Middle Market Activity

Which healthcare sub-sectors are seeing the most buyer and investor interest in the lower middle market? We analyzed mandates from over 1,500 buyers on Axial, and ranked each sub-sector according to its relative share.

| Rank | Sector | Percent of Buyer Mandates |

|---|---|---|

| 1 | Home Health Services | 9.52% |

| 2 | Healthcare Software | 8.20% |

| 3 | Dental | 6.88% |

| 4 | Mental & Behavioral Therapy | 6.61% |

| 5 | Veterinary | 6.35% |

| 6 | Contract Manufacturing | 5.56% |

| 7 | Pharmaceutical Retail | 3.97% |

| 8 | Outpatient Care | 3.97% |

| 9 | Dermatology | 3.70% |

| 10 | Medical devices manufacturing | 3.70% |

Seven of the top ten sub-sectors, according to buyer demand, are retail service-based businesses.

The dominance of these retail service-based healthcare categories prompted an investigation into why the top three services categories in particular are most in demand:

Accompanying the data, we have included commentary and analysis from the active dealmakers on what they’re seeing and why they’re seeing it.

“PDGM [Patient Driven Groupings Model] is going to be big,” says Managing Director Bradley Smith of Vertess, a Texas-based healthcare focused M&A advisory firm.

PDGM is a new case-mix classification model used to structure healthcare payment categories and reimbursement thresholds. Come January 1, 2020, there will be a change in the unit of home health payment from a 60-day period to a 30-day period, forcing smaller providers to make substantial adjustments to their operating models.

“It will be similar to what happened in home health in 2000, and it will cause a massive consolidation. Similar to competitive bids that the DME [Durable Medical Equipment] market went through in 2009 and 2010, we are going to see a consolidation of a significant portion of the marketplace, creating opportunity for existing players and generating more PE interest. PDGM is a disruptive opportunity for them to execute a rollup strategy and capture a substantial part of the market,” says Smith.

“Home care will certainly come out of this PDGM issue with fewer operators in the market,” notes Cory Mertz, co-founder of Mertz Taggart, a healthcare M&A advisory firm focused on home and behavioral health. “I’m not sure how many, but I’ve heard estimates that as many as 30 percent of companies will come to market as a result of the cash flow shortage.”

For investors seeking new platform investments as well as entrepreneurs, it seems that the new threshold created by PDGM will determine whether they are above or below the minimum economies of scale. “Operators will realize they can’t make money doing the same thing over the last 10 years. They’ll be forced to adapt by either selling, merging, or raising capital, with the only other option being to go out of business or declare bankruptcy. And that puts acquisition activity and the market as a whole on steroids,” says Vertess’ Smith.

No one seems to disagree about PDGM’s ultimate impact on the category. However, perspectives diverge substantially more on when and to what extent activity will intensify. Many think that it will take at least one or two quarters for M&A activity to increase by forcing businesses to go to market, and an additional few quarters until we see the majority of buyers and investors becoming comfortable with deploying capital.

Activity in the near-term could also be stalled by the uncertainty of the future regulatory environment, which could create misaligned expectations between buyers and sellers. Even if more deals will come to market, given the expected declines in revenues and increased urgency of sale, we can expect to see a decline in valuations. The kind of structural shift represented by PDGM often results in a temporary freeze on activity, as business owners typically agree that consolidation is due, yet linger in denial about who should be consolidated or play a tug-of-war with buyers on valuation.

Says Neil Johnson, managing director at healthcare advisory firm Lawrence Evans & Co., “The unknown revenue reduction is causing buyers to restructure and reprice, which sellers don’t want to see. So we are in a bit of a holding pattern on those deals until after Q1 2020 due to that uncertainty.”

“Right now, it’s hard enough for a PE firm to get a handle on the [healthcare] industry in general, but then to figure out how PDGM might impact a target is very difficult,” notes Mertz’s Q3 Home Health report. “They have other opportunities they can look at for now until the dust settles in home health. I would look for private equity to jump back into the mix in the second half of 2020, barring any other unforeseen regulatory announcements.”

As for sellers, pressure is likely to grow on the weakest players to jump to the front of the queue, and take buyout offers at lower valuations for fear of missing out completely. The most savvy financial and strategic buyers will likely be rewarded with lower valuations for early takeouts, while tolerating more risky investments.

“High LTV ratios and low default rates drive PE interest in dental clinic consolidations (DSOs)”

What are the core factors driving investor and buyer appetite for dental consolidation? Doug Rozsa, CEO of dental, veterinary, and optometry M&A advisory firm FiSol DVO, suggests that it all comes down to really good potential for multiple expansion driving excellent returns.

Private equity firms “feel as though they can’t lose money even if they try, and for the time being, they’re not that far off,” Rozsa says. “Private equity funds are thinking that if they buy at a 4-8x or even a 10x multiple, they can grow it to a 14-16x multiple — and that’s good math. You get the right management team in place, and there’s a clear path to very healthy levels of EBITDA. And given the risk of default is so low, it’s not a bad bet from any PE firm if they find a multiple they can live with.”

FiSol is currently seeing cases in which $1-2M EBITDA dental businesses are receiving valuations at a 4-8X EBITDA multiple, $2-$5M EBITDA businesses at 8-10X, and businesses in the $5-$10M EBITDA range receiving multiples in the 10-12x range from motivated buyers and investors.

One of the primary drivers of these economics is the low default rate. Default rates below one percent are typically very attractive to capital providers, and the .50 percent default rate for dentist offices are an even greater standout. PE firms thus have additional upside to equity by adding substantial leverage in DSO rollups. For such steady cash flow businesses, crystallizing returns is largely a matter of banking the distributions over time.

Catalysts of the DSO Explosion

In 2008, private equity observed that consumer spending on dentistry — out of pocket, insurance or otherwise — was flat, while much of the rest of the industry was down. And the reports of default rates across banking portfolios showed a similar trend — dentistry portfolios remained relatively flat, while portfolios in almost every other healthcare sub-sector took a dive. “Most banks did not have a hard time with their dental portfolios during the recession,” says FiSol’s Rozsa. “Nothing is recession-proof, but dental proved substantially more resilient.”

Investors soon came to realize that dentist offices were adhering to a common, and very attractive, pattern: high loan-to-value (LTV) ratios and extremely low default rates.

Structured consolidation activity under the umbrella of “dental services organizations” started to accelerate about 4 or 5 years ago. Dental services organizations, or DSOs, are independent business support centers that provide business management and support to dental practices in the United States, and are the commonly used structure under which buyers structure dental rollups.

“Back in 2014 and 2015, probably somewhere around 15 percent of doctor’s practices were part of a DSO,” says Tusk Partners’ Kevin Cumbus. Tusk Partners is a leading M&A advisory firm focused exclusively on the dental space. “Doctors who built these groups or had these practices were subjected to information asymmetry — they were not really aware of the demand or what their business should be worth as part of a consolidation play for a bigger player. They were getting 2-3x and gladly accepting it, because it was substantially more than what another doctor would pay. This information arbitrage for investors still exists in today’s market.”

Today, interest in the space continues to rise. “Dental is still a relatively small market with a lot of growth opportunity. So the dynamic and influences for growth are great. As a result, financial investors and strategic buyers alike continue to have an insatiable appetite in the space,” says Rozsa.

“We are continuing to see an increase in the velocity of consolidation, and we fully expect the consolidation to continue. Our best estimate is that we’re only about 20-22 percent consolidated today,” says Tusk’s Cumbus.

At the end of the day, it all comes down to who’s running the business, what they are looking for, and whether the business is a better fit for a PE or strategic acquirer. Some dentists are exhausted and want to fully exit the business, while others are executing on a 5- or 10-year growth engine and looking for an operational partner to help them run faster.

“Mental and behavioral health rationalizing in overheated and crowded areas; continued growth in autism diagnoses point to more sustained category growth”

“In 2014 and 2015, it wasn’t uncommon to see 40-50 percent EBITDA margins in behavioral health categories, but the market crumbled a bit in 2016. With everybody and their brother wanting to get a piece of the action, there became a glut of beds in the category,” says Mertz.

With both patient recidivism rates and private equity-led activity in behavioral health at all-time highs during the mid-2010s, payers became more sophisticated and reduced reimbursement. This led to the current rationalization period, which many predict will last through 2020. The market for resource-intensive residential substance abuse programs has settled a bit, and is expected to take another quarter or two before it re-corrects as consolidators try to digest and stabilize what they’ve acquired over the last few years. `

In the meantime, “the MAT category is super hot with very high multiples,” remarks Kevin Taggart, co-founder of Mertz Taggart. MAT refers to “medically-assisted treatment centers,” which combine behavioral health with medicine to treat substance abuse disorders.

Within this category are OTPs (opioid treatment programs), which increasingly are moving away from inpatient care to a lower-cost care model wherein the patient receives daily doses of medicine administered at an office. These enable the patients to live functional lives, with patients in this category as a result representing 10-20 year customer lifetimes given current treatment protocols.

Part of the attraction of these MAT approaches is the contrast in their approach with legacy inpatient approaches, which focused on abstinence-based techniques. Inpatient approaches are not only more expensive but also suffer from enormously high failure rates, such that insurers must pay out for no sustainable patient benefit.

Autism Care Likely to Enjoy Regulatory and Political Steadiness

Autism diagnoses have more than doubled in the last 10 years, from one in 125 children being diagnosed in 2008 to one in 59 in 2018, according to the Center for Disease Control and Prevention. Fifteen percent of that growth has come in the last two years. While theories abound regarding the causes of autism’s growth on an absolute basis (aging maternalism, pesticides, and other environmental factors), it still appears to be largely a hereditary disorder. As more cases are diagnosed, M&A opportunities and the overall category continue to expand.

Risk factors for the sub-sector are minimal. “The only meaningfully large player that could influence reimbursement in the autism category is maybe Tricare,” says Keith Jones, CEO of Blue Sprig Pediatrics, a leader in the autism services category. “We’re not really touched by PDGM-related issues. And as for the 2020 presidential election, it would likely be a political minefield to go after the Autism Cares Act.” The Autism Cares Act is the primary source of federal funding for autism research, services, training, and monitoring.

Given these trends, PE firms and sponsor-backed corporations are chomping at the bit for mental and behavioral healthcare opportunities, sometimes paying multiples in the low- to mid-teens for a businesses above $2 million EBITDA.

KKR-backed Blue Sprig continues to grow at a very rapid pace, both organically and through strategic acquisitions. “We maintain full conviction in the space, and believe that there is still a clear and significant need for a rational provider to exist at scale. We believe we’re well-positioned to be that provider.”

When it comes to healthcare in 2020, the trends of capital superabundance and the prevailing winds of regulatory change will continue to favor the specialists and subject matter experts who are best able to underwrite and price risk in the changing healthcare economy.

For advisory firms, we are seeing firms with expertise in specific healthcare sub-sectors gaining an edge: Tusk Partners in dentistry; Mertz Taggart in home and behavioral health; FiSol in dentistry, veterinary and optometry; and both Lawrence Evans and Vertess laser-focused on specific healthcare sub-verticals that align with each senior director’s unique experience. Several of these firms have already seen an increase in inbound demand from ready and prepared healthcare sellers looking to initiate a quick process before the market potentially chills.

“We are getting more of our fair share” of inbound interest from sellers, says Vertess’ Brad Smith. “Even though baby boomers looking for exits are still creating substantial M&A tailwinds, and valuations are still high, it’s in part attributable to us… Vertess has gone a mile deep and an inch wide in an enduring industry that will continue to be very active from an M&A perspective.”

For buyers and investors, the edge will go to firms whose healthcare expertise allows them to be bold in taking advantage of opportunities early in the 2020 cycle.

For some sectors, such as dental services and healthcare practitioners, the more healthcare-savvy investors will be able to present sellers with slightly higher valuations and multiples that win them deals while confidently leaving enough runway for growth. In other industries such as home health, more risk-tolerant expert investors will be able to take advantage of PDGM-induced activity at the right time — beating other investors to yield favorably low valuations, while entering markets after they’ve ascertained how the regulatory issues will impact respective business models. In mental and behavioral health, understanding of an investment target’s economies of scale relative to competitors will determine success, as well as investors’ exposure to services with tighter or changing reimbursement policies.

The market at the onset of 2020 will be poised for more M&A opportunities as a whole —especially for the more knowledgeable and/or risk-tolerant investor. Advisors are expecting a disproportionate share of M&A activity to take place in industries less impacted by regulations, such as dentistry, while uncertainty about the regulatory environment and its financial implications in other sectors such as home and behavioral health is expected to decelerate both investor and seller activity until mid-2020.